Chrisman Commentary - Daily Mortgage News

The Chrisman Commentary podcast provides daily insights into the mortgage industry, covering market trends, capital markets, and regulatory changes. Hosted by Robbie Chrisman, each episode delivers expert analysis and industry perspectives on the forces shaping housing finance. Whether it’s mortgage rates, lending news, or economic shifts, the podcast offers a clear, concise breakdown of the most important developments. More at www.chrismancommentary.com.

Chrisman Commentary - Daily Mortgage News

2.23.23 FHA Mortgage Insurance Premium Cut; Alexandra Nolan on Entrepreneurship; Federal Reserve Minutes

Thanks to Agile, bringing the mortgage capital markets into a new digital era. From lenders to dealers, Agile is the new way to quote MBS.

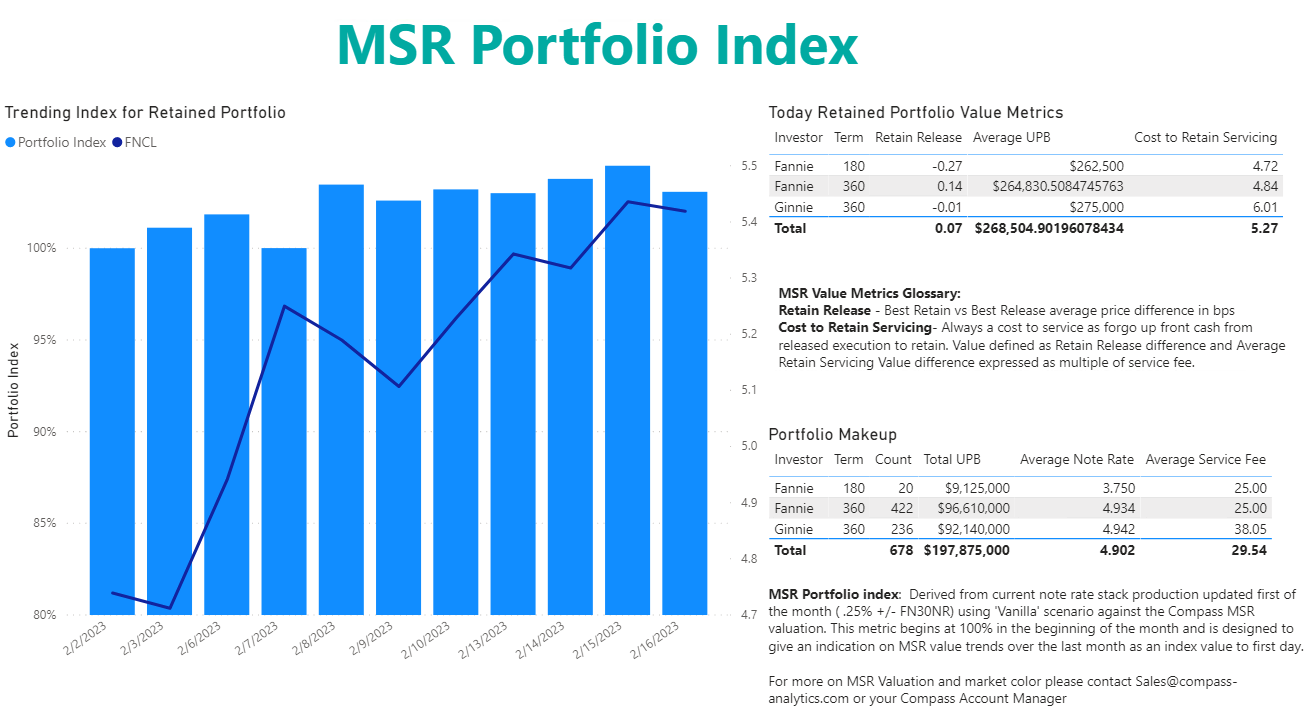

Remember, not all math puns are terrible...just sum. Analyzing residential servicing is a combination of math and psychology. If you were an institution thinking of buying mortgage servicing rights (MSR), or a lender running the numbers on retaining servicing rather than selling it to an aggregator like AmeriHome or Penny Mac, you don’t like hearing the saying, “Marry the house, date the rate.” You’d prefer that the loan stay “on your books” well into the future because you want the monthly cash flow. In 2020 and 2021 origination income was dominant. But in 2022 servicing income won the day for those who owned it. What will happen to servicing in 2023? No one has a crystal ball, but if rates stay in the 5’s or 6’s, loans funded in 2020 and 2021 still stick. Prepayments have plummeted: no one wants to pay off their 2.875 percent loan. Of course, there are numerous parties slicing and dicing the numbers. For example, Black Knight’s MSR Index takes a sample current note rate production portfolio and tracks the MSR performance throughout the month by comparing the current value to the first day of the month value. (Today’s podcast can be found here and this week’s is sponsored by Agile, bringing the mortgage capital markets into a new digital era. From lenders to dealers, Agile is the new way to quote MBS. Listen to an interview with entrepreneur and author Alexandra Nolan on launching and growing a successful business.) Jobs and transitions___________________________________________________ “It’s evident that the mortgage industry is grim with many lenders closing their books with net losses for 2022. All Originators, both rookies and veterans, are holding their breath waiting for interest rates to drop, but why? It’s not about rate, it’s about partnering with a lender that can give you the tools to succeed in a down market. InterLinc was built on sustainability, strong business values & a profitable P&L. As a high-service lender with a high-touch, boutique feel, we are proud to close our 2022 books with a very respectful profit compared to the industry. Key strategies have allowed Originators to earn more business with less time, notably marketing advancements improving the Customer Experience, technology that allows loans to close quicker and faster. Don’t let 2023 be the year that knocks you to your knees, react to the challenges by partnering with a lender has the tools & leadership for you to succeed. Email James Durham for a confidential conversation.” “Button Finance, your Home Equity Loan partner, is seeing explosive growth and is looking to grow its team with an experienced Account Executive. We have expanded our product offerings and now offer up to 3% broker compensation! Our industry-leading pricing portal allows your clients to lock loans automatically and our operations team can CTC a loan within five business days. This is a unique opportunity to join a growing company solely focused on being one of the top 2nd-lien lenders in the nation. If you’re a self-starter with existing broker relationships and want to continue to grow with us, this is the right place for you. Compensation includes salary, equity in Button Finance, and up to 35bps commission. Please send your resume to Rose King.” “Ready to take your pipeline to new heights? We’ve got you covered! Coast One Mortgage, a part of the Newrez Family of Companies, is looking to grow its team with more ambitious Loan Officers in Florida, Michigan, and Ohio and Area Sales Managers in Port Charlotte and Port St. Lucie, Florida. “Coast One Mortgage is committed to creating a top-tier experience for our borrowers and to growing core markets by leveraging our Joint Venture Real Estate partner and other strong local real estate professionals. Our platform offers a wide product breadth, including but not limited to Non-QMs (Jumbo, Self-Employed, Investor, Non-Warrantable Condo’s), Jumbo loans with only 3.5% down payment, no mortgage insurance, and all the traditional financing options,” said Marty Garrity, President of Coast One Mortgage. Join our team of experienced Loan Officers and Area Sales Managers today! For more information on Coast One Mortgage or Newrez, get in touch with Marty Garrity or our recruiting team.” Thrive Mortgage has been making waves in the mortgage industry with its innovative products and customer-focused approach for more than 22 years. The company is consistently ranked as a top mortgage company in the industry and has won numerous awards for its commitment to customer service. One of Thrive’s standout products is its Home2Home program, which allows borrowers to close on their new home without selling the departing residence in one transaction. This innovative program streamlines the buying and selling process making it easier for borrowers to upgrade to their dream home. “Thrive Mortgage's success is driven by our commitment to our customers and a focus on building strong relationships,” stated Selene Kellam, Thrive’s newly minted CEO. “By prioritizing communication and transparency, we have built a loyal customer base and a reputation for excellence.” To inquire on available growth opportunities in your market, contact us or visit us. LoanWyse appointed Paul Howarth as the EVP of Production, responsible for overseeing the company’s national expansion across all origination channels. “LoanWyse has been at the forefront of developing proprietary technology for the non-QM mortgage space, and this was the biggest reason I decided to join the organization.” (“LoanWyse dba of Optionwide Financial Corporation, was founded to help redefine how Non-QM loans are originated and processed.”) OriginPoint, a mortgage origination joint venture between Guaranteed Rate Inc. and Compass, has appointed four new Divisional Managers to oversee sales across the country: Anita Pereda who oversees the Northwest division, Joe Kolesar in the Central division, John McGinty in the Eastern division, and Komron Tarkeshian in the Southwest. Lender and broker services & products___________________________________________________ Are you tired of having to adjust head count every time the market changes? The Mortgage Automation Suite, brought to you by Richey May and Zoral, can help. With scalable automated solutions that improve accuracy while reducing repurchases and costs, your business will be well-equipped for any market cycle. Leveraging this powerful automation will allow your team to close loans more easily, helping to retain your best staff. Plus, it adds the extra layer of stability needed during difficult times; something we could all use a bit more of these days! Find out how the Mortgage Automation Suite from Richey May & Zoral can help you today. Email us. Make loan quality your top priority in 2023 with this playbook! With the market changes forcing everyone to take a hard look at their business, now is the time to identify the best lines of defense for maintaining loan quality and mitigating risk. Look no further than your servicing revenue to carry you through the current down cycle. In this playbook, you'll discover the three key lines of defense for maintaining servicing loan quality and how you can refine each to optimize asset performance, maintain compliance, and deliver superior customer service. Read Now. “Times like these demand experience, flexibility and staying power. We know: we’ve been here for 30 years. Clayton is a leading provider of due diligence, underwriting and risk mitigation solutions with the scale and expertise to handle any size residential or commercial engagement, ensuring assets and processes meet quality, compliance and reporting standards and comply with regulatory, rating agency and investor requirements. With more than 17 million loans reviewed and $2 trillion in loans / MSRs monitored, we're ready for what's next...are you? Visit us at booth 93 next week at SFVegas 2023 or contact Clayton’s VP-Business Development Tom Coffey to learn more.” In TPO news, aMortgage Boutique, a division of First Community Mortgage recently announced the launch of the HomeZero 100% FHA DPA program. This innovative program provides borrowers with the opportunity to purchase a home with no down payment, making homeownership achievable for many who would otherwise be excluded. The HomeZero program offers two flexible options for the second lien, a fully amortizing second lien at a rate 2% above the note rate on the first lien, or a forgivable second lien that becomes forgivable after 10 years. This flexibility allows borrowers to choose the solution that best fits their financial needs. At aMortgage Boutique, we understand how important your customers, referral partners, and your reputation are on every loan. Our commitment to competitive pricing, along with our excellent service levels, sets us apart from other lenders. For more information on the HomeZero DPA program, contact Jeff Raich. If your loan originations are drying up in the current housing market drought, you need to get the most out of every opportunity. And the best way to ensure that loans move from application to close is by elevating your customer experience and providing a smooth, seamless process that not only turns today’s borrower into tomorrow’s refinancer, but also boosts your productivity and efficiency, so you can engage with more customers. Total Expert’s recently expanded integration with Encompass makes it easier to wield your data, personalize the customer journey, and maximize loan conversion. Create loan files directly in Total Expert with one click, sync contact and historical data, and receive real-time updates from Encompass to seamlessly trigger workflows and marketing automation. Schedule time to connect with our team, or come find us at the upcoming ICE Experience event in Las Vegas from Feb 27-March 1. Do you want to get in front of top clients and referral sources and generate immediate business? Check out the StorySeller Virtual Summit on April 19-20. The event is hosted by Gibran Nicholas, who will interviewing several big-name speakers about how to grow business and build your personal brand using StorySelling. A marketing partnership would be a good fit if: (1) You want to put on a world-class, super-unique “wow” experience for clients and referral sources without tying up any of your internal resources; (2) You want your company’s branding to show up exclusively whenever someone logs into the virtual event using your link; and, (3) You want to generate high-quality leads and close immediate business. If you’re a potential marketing partner who can drive at least 1,000+ attendees to a free virtual event like this, email Gibran directly to learn more about a private-label marketing partnership. HousingWire recently dubbed the borrower intelligence platform (BIP) “the most essential addition to the mortgage tech stack since the advent of the loan origination system,” and the TrustEngine BIP is leading the pack. Must-have technology for every lender, TrustEngine BIP amplifies existing LOS, POS and CRM systems to identify more leads, deepen borrower relationships and get loans to the finish line. Not to be confused for standard borrower intelligence alerts and triggers, the TrustEngine BIP supports comprehensive behavior analysis to facilitate more relevant borrower outreach. Stop wasting money on technologies your LOs aren’t even using. Contact TrustEngine today to start maximizing all the tools in your toolbox. STRATMOR on wealth management borrowers___________________________________________________ Mortgage lenders in search of new business could find it by partnering with private bankers and wealth managers who serve High Net Worth (HNW) borrowers, according to the just-released February issue of STRATMOR Group’s Insight Report. In her article, “At the Intersection of Mortgage Lending and Wealth Management,” STRATMOR Principal Jennifer Smith notes that there is a lot of upside to working with HNW borrowers. “Lenders can make the same amount of money — or more — with fewer deals because the loan sizes are larger, loan officers will likely receive a steady stream of qualified borrowers, and the fulfillment team will see very clean credit with good liquidity,” says Smith. In the article, Smith analyzes this business segment and outlines how lenders can approach building the trust that fuels a relationship between mortgage and wealth management. Check out her article in the February Insights Report. Not everyone is excited by the FHA MIP cut___________________________________________________ As noted in the Commentary early yesterday morning, the Biden administration announced a 30bp cut in the mortgage insurance premium (MIP) for FHA borrowers. It is important to note MIP is paid on top of the mortgage rate, so the cut will have no effect on best execution for lenders. This will certainly impact affordability for lower income borrowers, but most think it will have little effect on prepayment speeds in the short run. In even more of a primer, the MIP is a monthly fee that homeowners with FHA-insured mortgages pay to insure their mortgages, paid on top of their monthly principal and interest payments. Based on the average FHA mortgage amount of around $270,000, borrowers would see significant savings of approximately $800 annually. This reduction in MIP will lower housing costs for an estimated 850,000 homebuyers and homeowners in 2023. Good news, right? Not so fast. Seth Appleton, President of U.S. Mortgage Insurers (USMI, that works primarily with Freddie and Fannie), stated, after a nod to removing barriers to home ownership and FHA’s role in it, “The decision to reduce annual premiums on FHA-insured mortgages is well-intended but could result in unintended consequences for both the FHA and the borrowers it seeks to serve. For borrowers, FHA’s pricing action may make homebuying more challenging by driving up home prices even more and impairing the ability of low- and moderate-income, first-time, and minority borrowers to access homeownership. For the FHA, reduced premiums decrease its fiscal resiliency in an environment of economic uncertainty and volatile interest rates.

“FHA’s pricing policies should be actuarially sound and promote prudent long-term risk management that allows it to weather all economic scenarios in order to support future borrowers. Given the volatility in the housing market, the FHA must be prepared for the risks associated with an increase in defaults and depreciation of home values while retaining the capacity to play its important countercyclical role. It is also important to ensure the taxpayer-backed FHA market operates in a consistent and coordinated manner with the conventional market, which provides access to affordable homeownership with private capital that protects taxpayers from undue credit risk.”

Capital markets: the strong labor market continues___________________________________________________ The FHFA announced on 1/12/2023 that they will require the GSEs to establish and implement risk management policies and procedures for monitoring and valuing MSRs. MCT can help you develop the appropriate strategy to make sure you are prepared in advance of the April 1, 2023 effective date. Whether you’re looking for a second opinion on your periodic valuations, evaluating the necessity of more frequent MSR valuations, or considering if now is an opportune time to sell, MCT has expertise to provide guidance. Learn more about MCT’s MSR Services or contact MCT today for more information. In addition to a top-notch MSR Services team, MCT provides guidance when you need it the most. MarketFlash updates, client-exclusive webinars, new product/service announcements, and MCT University are just a few examples of content-driven support. Sign up for MCT’s newsletter to receive the latest industry news and insights. Moving on to bonds, we finally had some relief from the recent rise in rates yesterday, because even a dead cat bounces when it hits the sidewalk, right? (Sorry Myrtle, that’s trader talk.) The Minutes of the most recent meeting of U.S. Federal Reserve officials indicate further rate hikes, with most supporting a slower pace. Recessionary concerns were also raised with some participants seeing elevated prospects of a recession this year. St. Louis Fed President Bullard, a noted hawk, said yesterday morning that markets have overpriced the chance of a recession and that the Fed Funds rate range will have to be lifted past 5.00 percent to tame inflation. Today’s calendar included a busy start with the second look at Q4 GDP (2.7 percent compared to the 2.9 percent expected), and weekly jobless claims (192k versus last week’s 200k; 1.654 million continuing claims). The Core PCE Deflator was 4.3 percent. Later this morning brings KC Fed manufacturing, a Treasury auction of $35 billion 7-year notes, Freddie Mac’s latest Primary Mortgage Market Survey, and remarks from two Fed presidents, Atlanta’s Bostic and San Francisco’s Daly. We begin the day with Agency MBS prices worse .125-.250, the 2-year yielding 4.72, and the 10-year yielding 3.97 after closing yesterday at 3.92 percent. From Indiana, Carol K. writes, “The fact that some people can’t distinguish between etymology and entomology bugs me in ways I can’t put into words.”

{kind=link}